Understanding Like-Kind Property in 1031 Exchanges

Understanding Like-Kind Property in 1031 Exchanges: Essential Rules and Investor Guidance

Navigating the complexities of real estate investment can be daunting, especially when it comes to understanding the nuances of like-kind property in 1031 exchanges. This article aims to demystify the IRS definition of like-kind property, explore which properties qualify, and provide practical guidance for investors. By grasping these essential rules, investors can leverage 1031 exchanges to defer capital gains taxes and optimize their real estate portfolios. We will delve into the IRS criteria, the impact of recent tax legislation, and strategic considerations for successful exchanges. Additionally, we will highlight how The 1031 Group supports real estate investors in making informed decisions regarding like-kind property.

What Is the IRS Definition of Like-Kind Property in a 1031 Exchange?

The IRS defines like-kind property as property of the same nature or character, even if they differ in grade or quality. This broad definition allows for a wide range of real estate assets to qualify for 1031 exchanges, provided they meet specific criteria. Understanding this definition is crucial for investors looking to maximize their tax deferral benefits through strategic property exchanges.

How Does the IRS Define 'Like-Kind' for Real Estate Exchanges?

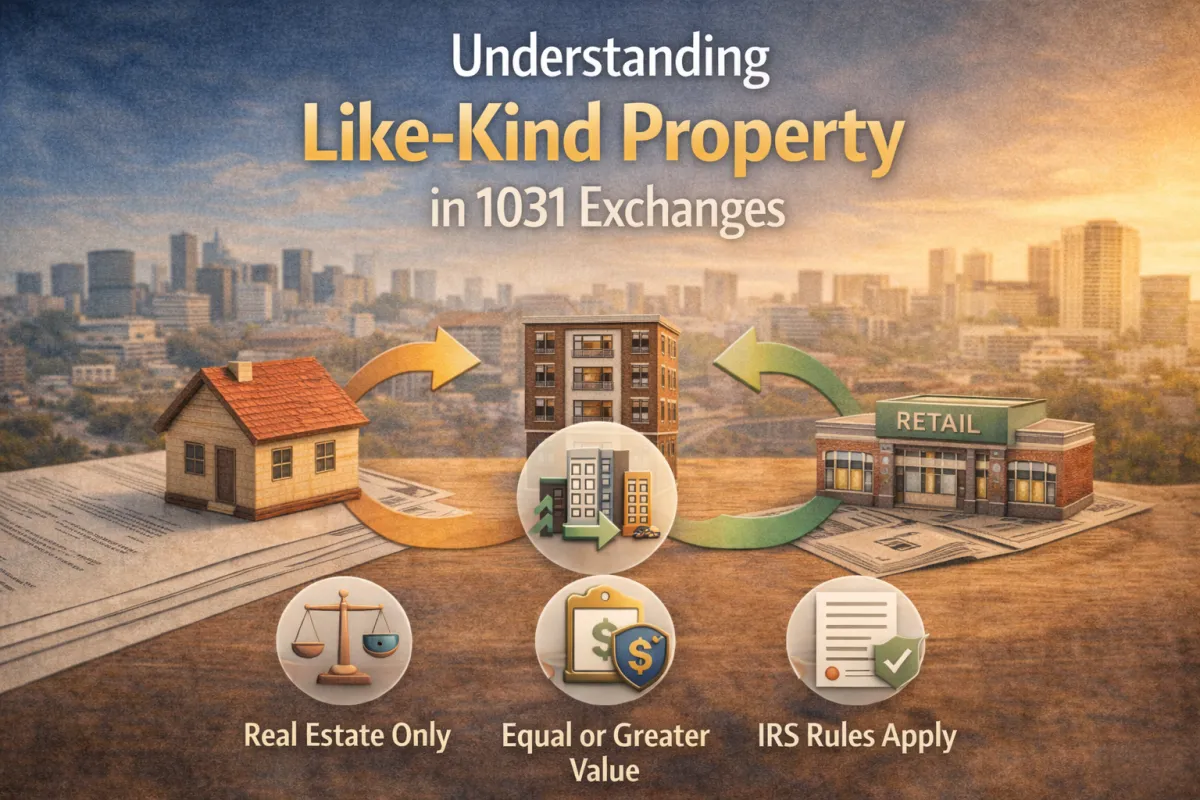

According to IRS guidelines, like-kind property encompasses various types of real estate, including residential, commercial, and industrial properties. For instance, an apartment building can be exchanged for a retail space, as both are considered real estate. The key factor is that the properties must be held for investment or productive use in a trade or business. This flexibility allows investors to diversify their portfolios while deferring taxes on capital gains.

What Was the Impact of the 2017 Tax Cuts and Jobs Act on Like-Kind Property?

The Tax Cuts and Jobs Act (TCJA) of 2017 significantly impacted the landscape of like-kind exchanges by limiting the definition to real property only. Prior to this change, personal property could also qualify for 1031 exchanges. As a result, investors must now focus solely on real estate transactions to benefit from tax deferral. This shift emphasizes the importance of understanding the current regulations to ensure compliance and maximize investment opportunities.

Which Real Estate Properties Qualify as Like-Kind for 1031 Exchanges?

Identifying which properties qualify as like-kind is essential for investors looking to execute successful exchanges. The IRS allows a variety of real estate assets to be exchanged, provided they meet the necessary criteria.

What Types of Investment and Business Properties Are Eligible?

Eligible properties for 1031 exchanges include a wide range of investment and business properties, such as:

Residential Rental Properties: Single-family homes, multi-family units, and apartment complexes.

Commercial Properties: Office buildings, retail spaces, and warehouses.

Industrial Properties: Factories and manufacturing facilities.

These properties must be held for investment or business use, ensuring that they are not primarily for personal use.

How Do Delaware Statutory Trusts Qualify as Like-Kind Property?

Delaware Statutory Trusts (DSTs) are increasingly popular among investors as a means to participate in 1031 exchanges. A DST allows multiple investors to pool their resources to invest in larger real estate projects, such as commercial buildings or multifamily complexes. The IRS recognizes DST interests as like-kind property, provided they meet specific requirements, including being structured as a trust and having a qualified intermediary facilitate the exchange. This structure offers investors a unique opportunity to diversify their portfolios while benefiting from the tax advantages of 1031 exchanges.

What Property Types Do NOT Qualify as Like-Kind in 1031 Exchanges?

While many properties qualify for 1031 exchanges, certain types are explicitly excluded from eligibility. Understanding these exclusions is vital for investors to avoid costly mistakes.

Why Are Personal Residences and Vacation Homes Excluded?

Personal residences and vacation homes do not qualify as like-kind property under IRS regulations. The IRS stipulates that properties must be held for investment or business purposes to be eligible for 1031 exchanges. This exclusion means that homeowners cannot defer taxes on the sale of their primary residence or vacation properties, emphasizing the need for investors to focus on investment-grade real estate.

Which Non-Real Estate Assets Are Ineligible for Like-Kind Exchange?

In addition to personal residences, non-real estate assets such as stocks, bonds, and other securities are also ineligible for 1031 exchanges. The IRS specifically limits like-kind exchanges to real property, reinforcing the importance of understanding the types of assets that qualify. Investors should be cautious to ensure that their exchanges involve only eligible real estate assets to maintain compliance with IRS regulations.

How Can Investors Apply Like-Kind Property Rules in Practical 1031 Exchange Scenarios?

Applying the rules of like-kind property in practical scenarios can help investors maximize their tax deferral benefits. Understanding the nuances of these rules is essential for successful exchanges.

Can Different Types of Real Estate Be Exchanged as Like-Kind?

Yes, different types of real estate can be exchanged as like-kind, provided they meet the IRS criteria. For example, an investor can exchange a commercial property for a residential rental property, as both are classified as real estate. This flexibility allows investors to adapt their portfolios to changing market conditions and investment strategies while deferring capital gains taxes.

What Are Common Misconceptions About Like-Kind Property?

One common misconception is that properties must be identical to qualify as like-kind. In reality, the IRS definition is much broader, allowing for various types of real estate to be exchanged. Another misconception is that personal use properties can qualify, which is not the case. Understanding these misconceptions is crucial for investors to navigate the complexities of 1031 exchanges effectively.

What Strategic Considerations Should Investors Know About Like-Kind Property?

Investors should be aware of several strategic considerations when dealing with like-kind property in 1031 exchanges. These factors can significantly impact the success of their investment strategies.

How Does Understanding Like-Kind Property Affect Tax Deferral Benefits?

A thorough understanding of like-kind property is essential for maximizing tax deferral benefits. By strategically selecting properties that qualify for 1031 exchanges, investors can defer capital gains taxes and reinvest their profits into new properties. This approach not only enhances cash flow but also allows for portfolio growth without the immediate tax burden.

What Is the Role of Intent and Documentation in Qualifying Property?

Intent and proper documentation play a critical role in qualifying properties for 1031 exchanges. Investors must demonstrate that the properties are held for investment or business purposes, which can be established through documentation such as rental agreements, property management records, and financial statements. Maintaining clear records and demonstrating intent is essential for compliance with IRS regulations and successful exchanges.

How Does a Qualified Intermediary Facilitate Compliance in Like-Kind Property Exchanges?

A Qualified Intermediary (QI) is a crucial component of the 1031 exchange process, ensuring compliance with IRS regulations and facilitating smooth transactions.

Why Is a Qualified Intermediary Required for 1031 Exchanges?

The IRS requires the use of a Qualified Intermediary to facilitate 1031 exchanges to ensure that investors do not have direct access to the proceeds from the sale of their relinquished property. The QI holds the funds in escrow and manages the exchange process, ensuring that all legal requirements are met. This requirement helps maintain the integrity of the exchange and protects the tax-deferred status of the transaction.

How Does Coordination with Advisors Enhance Exchange Success?

Coordinating with financial and legal advisors can significantly enhance the success of 1031 exchanges. Advisors can provide valuable insights into market conditions, property valuations, and tax implications, helping investors make informed decisions. By leveraging the expertise of professionals, investors can navigate the complexities of like-kind exchanges more effectively and optimize their investment strategies.

Property Type Qualifying Criteria Examples:

Residential Rental, Held for investment, Single-family homes, multi-family units, Commercial PropertyHeld for business, Office buildings, retail spaces, Industrial Property, Productive use Factories, warehouses

This table illustrates the various types of properties that qualify for 1031 exchanges, highlighting the flexibility investors have in selecting like-kind assets.

Investors must remain vigilant in understanding the nuances of like-kind property to maximize their tax deferral benefits. By leveraging the expertise of The 1031 Group, real estate investors can navigate the complexities of 1031 exchanges and make informed decisions that align with their investment goals.

Visit our Website

Subscribe to our Newsletter

Join our Online Community

Book a Strategy Call with one of our Advisors